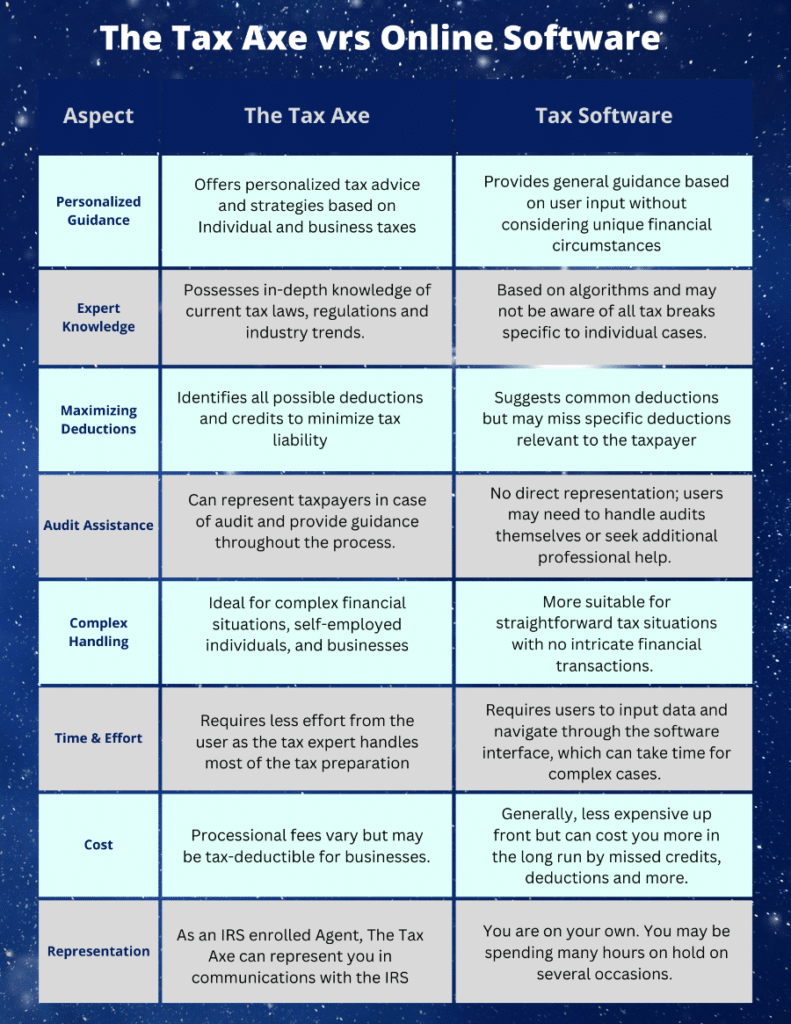

When it comes to saving money on your taxes, two terms you’ll hear often are tax credits and tax deductions. While both reduce the amount of taxes you owe, they work in different ways. Understanding the difference between the two and knowing how to use them can help you maximize your tax savings. Let’s break down tax credits and deductions to help you determine which one can save you more money.

What’s the Difference Between a Tax Credit and a Tax Deduction?

-

Tax Deduction: A tax deduction reduces your taxable income. For example, if you’re eligible for a $1,000 deduction, it lowers your taxable income by $1,000, which in turn reduces the amount of taxes you owe. The value of a deduction depends on your tax bracket. For instance, if you’re in the 22% tax bracket, a $1,000 deduction would save you $220 in taxes (22% of $1,000).

-

Tax Credit: A tax credit directly reduces the amount of tax you owe, dollar for dollar. If you qualify for a $1,000 tax credit, your tax liability is reduced by exactly $1,000. This makes tax credits generally more valuable than deductions, as they provide a more direct reduction in your tax bill.

Types of Tax Credits

-

Nonrefundable Tax Credits:

These credits can reduce your tax liability to zero, but not below zero. In other words, if you owe $500 in taxes and you qualify for a $1,000 nonrefundable tax credit, your taxes will be reduced to zero, but you won’t receive a refund for the excess $500. Examples of nonrefundable credits include the Child Tax Credit (in some cases) and the Lifetime Learning Credit. -

Refundable Tax Credits:

Refundable tax credits can reduce your tax liability to below zero, meaning you can receive a refund even if you don’t owe any taxes. One of the most well-known refundable tax credits is the Earned Income Tax Credit (EITC), which provides assistance to low- and moderate-income workers. -

Partially Refundable Tax Credits:

Some credits are partially refundable, which means you can get a refund for part of the credit if it exceeds your tax liability. The American Opportunity Tax Credit for education expenses is an example of this.

Which is More Valuable: Tax Credits or Tax Deductions?

While both tax credits and deductions are valuable, tax credits typically provide a greater benefit because they directly reduce the amount of tax you owe. For example, if you qualify for a $1,000 tax credit, it will reduce your tax bill by $1,000, while a $1,000 deduction might only reduce your taxes by $220 if you’re in the 22% tax bracket.Tax credits offer a more direct reduction in your tax bill, which makes them more beneficial than deductions in most cases. However, deductions can still save you money by lowering your taxable income. To maximize your tax savings, it’s important to take advantage of both credits and deductions wherever possible. If you need help determining which credits and deductions apply to your situation, The Tax Axe is here to assist you in getting the most out of your tax return.

Navigating tax season can be challenging, especially with the prevalence of misinformation. By debunking these common tax myths, you can make more informed decisions and avoid unnecessary pitfalls. Whether you’re filing your taxes yourself or working with a tax professional, it’s essential to stay informed and proactive. For personalized advice and assistance, don’t hesitate to reach out to a qualified tax professional who can help you navigate your unique situation.