Dealing with back taxes can be a daunting task, especially as you approach the end of the year. Whether you’ve missed a payment or have an outstanding balance from previous years, it’s important to address back taxes promptly to avoid additional penalties and interest. As we enter September, this is a perfect time to take control of your tax situation and develop a strategy to manage and resolve your back taxes. Here are some steps to help you get started.

1. Understand Your Tax Liability

Before you can tackle your back taxes, you need to have a clear understanding of what you owe. This involves gathering all relevant tax documents and notices from the IRS or your state tax agency. Here are the steps to take:

Review IRS Notices

The IRS sends various notices and letters to inform taxpayers of their outstanding tax liabilities. These notices will detail the amount owed, including any penalties and interest. Review these documents carefully to understand the total amount due.

Access Your Tax Account Online

The IRS provides an online tool where you can view your tax account information, including your balance and payment history. Accessing this information online can give you a comprehensive overview of your tax situation.

Consult a Tax Professional

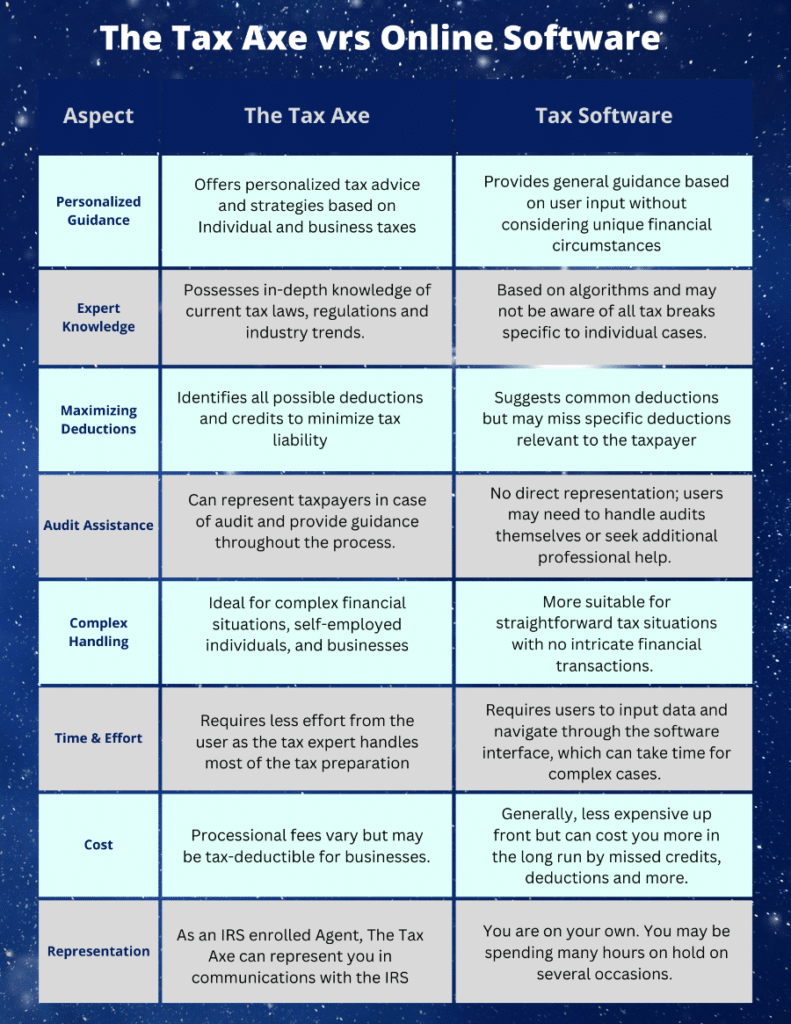

If you’re unsure about the details of your tax liability, consider consulting a tax professional. An experienced tax agent, like those at The Tax Axe, can help you decipher IRS notices and provide a clear picture of what you owe.

2. Evaluate Your Payment Options

Once you know how much you owe, the next step is to determine the best way to pay off your back taxes. The IRS offers several payment options to accommodate different financial situations.

Lump-Sum Payment

If you have the financial means, paying your back taxes in a lump sum is the fastest way to resolve your tax debt. This approach can help you avoid further interest and penalties.

Installment Agreement

If paying in full is not feasible, you can apply for an installment agreement with the IRS. This allows you to pay off your tax debt in monthly installments over a specified period. There are two types of installment agreements:

- Short-Term Payment Plan: Typically for balances under $100,000, this plan allows you to pay off your debt within 120 days.

- Long-Term Payment Plan: For balances under $50,000, this plan extends the payment period beyond 120 days and includes monthly installment payments.

Offer in Compromise (OIC)

An OIC allows you to settle your tax debt for less than the full amount you owe. This option is available if you can demonstrate that paying the full amount would cause financial hardship. Applying for an OIC requires thorough documentation of your financial situation and a detailed application process.

Currently Not Collectible (CNC) Status

If you’re facing significant financial difficulties, you may qualify for CNC status. This means the IRS temporarily suspends collection efforts until your financial situation improves. However, interest and penalties will continue to accrue during this period.

3. File Any Missing Tax Returns

If you have unfiled tax returns from previous years, it’s crucial to file them as soon as possible. The IRS requires all outstanding tax returns to be filed before considering any payment plans or settlement options. Filing missing returns can also help you avoid additional penalties.

Gather Necessary Documents

Collect all relevant documents, including W-2s, 1099s, and receipts for deductions and credits. If you’re missing any documents, you can request transcripts from the IRS.

Prepare and File Returns

You can prepare and file your tax returns yourself or seek assistance from a tax professional. Filing electronically can expedite the process and reduce errors.

4. Seek Penalty Abatement

The IRS may reduce or eliminate penalties if you can demonstrate reasonable cause for failing to pay or file on time. Common reasons for penalty abatement include serious illness, natural disasters, or incorrect advice from a tax professional.

Submit a Penalty Abatement Request

To request penalty abatement, you’ll need to provide a written explanation of your circumstances and any supporting documentation. A tax professional can help you prepare and submit this request to the IRS.

5. Monitor Your Tax Account

Once you’ve addressed your back taxes, it’s important to stay on top of your tax obligations to avoid future issues. Regularly monitor your tax account to ensure payments are applied correctly and to catch any discrepancies early.

Set Up Account Alerts

Many online tax accounts offer alerts and notifications to keep you informed of due dates and account changes. Setting up these alerts can help you stay proactive about your tax responsibilities.

Keep Accurate Records

Maintain detailed records of all tax-related documents, including payment receipts, correspondence with the IRS, and copies of filed returns. Organized records can simplify future tax filings and provide evidence if any issues arise.

Handling back taxes can be a challenging process, but by taking proactive steps, you can manage your tax liability and avoid further complications. September is an ideal time to assess your tax situation, explore payment options, and develop a plan to address any outstanding tax debts.

At The Tax Axe, we specialize in helping individuals and businesses navigate complex tax issues. Our team of experienced tax professionals is here to guide you through every step of resolving your back taxes. Contact us today at (678) 675-4268 to schedule your consultation and start planning for a brighter financial future!